The most important aspect of the deal that has replaced the promissory notes is not what it entails but what it does not entail. It does not involve a write off of any of the debt so that less would have to be repaid and interest burden on the debt lowered. It does not involve the European Stability Mechanism, in effect the EU, directly funding the banks which appeared to be the deal offered last June and it does not affect all the bank debt.

The most important aspect of the deal that has replaced the promissory notes is not what it entails but what it does not entail. It does not involve a write off of any of the debt so that less would have to be repaid and interest burden on the debt lowered. It does not involve the European Stability Mechanism, in effect the EU, directly funding the banks which appeared to be the deal offered last June and it does not affect all the bank debt.

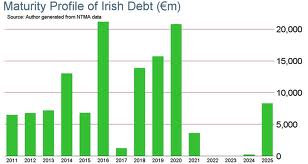

The deal on the promissory notes affects €28 billion of a total debt at the end of last year of €192 billion and relates to less than half that incurred in bailing out the banks. The Government has not changed its austerity targets. The editorial in the Financial Times stated that ‘restructuring the promissory note does not make the public liability for bank losses lower, just easier to bear.’ Easier to get workers to pay is more accurate. All the questions regarding how the deal will work have not been answered, which also demonstrates continuity with the promissory note arrangements that were understood fully by very few despite the enormous impact on people’s lives.

Never mind, the Taoiseach proudly told us that the “stains on our international reputations and dents to our national pride, have now been removed from the financial and political landscape”. This is a statement so revealing of the shallow moral argument for the deal, so instructive of the concerns of the elite as distinct from the majority and illuminating of the poisonous demands of national identity that despite its odious character it would be good to see it repeated again and again and again. The Irish people have decades to ponder how satisfying it is to pay for so long to erase such an embarrassment.

As for the new deal itself, it involved the liquidation of IBRC, which was the combination of Anglo-Irish bank and the Irish Nationwide building society. The Government will still pay €1bn to the bondholders of Anglo, as part of the 2008 guarantee, so no bondholder is left behind, and more rotten loans in Anglo will transfer to NAMA, which promises further losses down the road. Loans left in Anglo totalled €15bn.

It involves tearing up the promissory notes that provided the means for the State to get money from the Irish Central Bank (ICB), the local branch of the European Central Bank (ECB), to be replaced by ordinary government bonds, which are really just a more regular IOU used by states. This allows the state to keep the money loaned to it on the back of the promissory notes instead of having to pay it back when the notes were torn up. The state will still have to pay the money back and pay interest but will have much longer to pay and with what appears a lower rate of interest. Both of these are good things – having longer to repay and being charged less for the loan, but both are not as good as they appear.

The longer you have to pay the more you have to pay back, just like any mortgage. The lower interest rate is not such a change for the reason explained in the last article. This is because the high rate of interest paid by IBRC (8.2 per cent) to the Irish Central Bank, which the taxpayer ultimately funded, was used by the ICB to pay the ECB which charged a much lower rate of interest. The difference was returned to the Irish State so the effective rate of interest was not they headline rate of the promissory note. The reduced interest cost between the promissory notes and the government bonds is therefore not what it might appear.

But this is not the only reason the savings might not be so great. The ICB will have an asset, the bonds, the ownership of which entitles it to receive interest every year and receive repayment of the principal. Part of the deal is that the bonds are sold to private capitalists, €6.5 must be sold by 2022. How quickly they must be sold is not at all clear and thus neither is the cost of the deal, although this has not prevented the Government, media and commentators continuing to welcome the deal and proclaim its savings as if they were hard fact.

In selling the bonds the Government will in effect be raising new loans. If for example it attempts to sell €1bn worth of these bonds and investors don’t think the interest they would get on them is high enough they may be willing only to pay €980m, €950m or €930m instead of the €1bn. In other words the bonds would be sold at a loss and the tax payer would foot the bill. To replace the loss would require more loans costing more.

The rate of interest charged on the bonds over their lifetime is not known so calculations of how much the new deal will cost must make more or less educated guesses of how much the deal will actually cost over the long term. The longer the term the more the ‘educated’ guess becomes ‘pure’ guesswork.

Nevertheless within a couple of days estimates of savings on an NPV basis were quoted and savings of €8bn announced. Net Present Value (NPV) analysis allows one to calculate and compare amounts over different time periods recognising that someone would rather pay €1 in 10 years’ time than pay €1 today. It allows one to say whether it would be better to pay €1 for each of the next 9 years and €11 the following year or pay €2 for the next 10 years. In both you pay €20.

The money paid in the future is discounted so that €1 paid in ten years’ time is less than €1 paid in 5 years’ time which is calculated as less than €1 paid in 3 years’ time. How much you reduce the amount depends on the discount rate and this rate can have a big effect on the result. The rate chosen is another variable that is a guess, first educated and then pure.

The higher the discount rate the less costly future costs become which offsets the fact you are paying longer and on the face of it more. So one could be paying €21bn equally over 20 years instead of €19bn equally over 12 years but because the first means the money is paid off later it is worth less and the total cost on an NPV basis is less. In the example above an NPV calculation at a discount rate of 6 per cent shows that the first payment schedule costs €11.2 in NPV terms, where €11 is paid in the last year, and €14.7 in the second where equal yearly payments of €2 are made.

In the new deal the first repayment of principal is not until 2038 and the last in 2053. The NPV savings in the new deal were worked out by one economist as €8bn and then by a couple of others as €4bn, a whopping difference of 50 per cent of the first estimate. Another economist has stated that almost all of the calculated savings disappear if the timing of the sale of the government bonds to the private sector is accelerated. Factor in the loss on sale to the capitalists plus increased interest costs and the deal might very well cost more.

A final argument has been much quoted, and certainly more often than the lack of robustness of the savings estimates. This is that inflation will erode the real value of debt repayable by our children, who will be middle aged when they might finally pay it off. This means that, if say the interest rate is 5 per cent and inflation is 3 per cent the effective rate of interest is only 2 per cent. Also the real value of the money repaid in thirty years’ time will be less because of the cumulative reduction in the real value of the debt by this inflationary process.

It might otherwise be amusing to listen to these experts, who gave us a property ‘soft landing’ and now the wonderful benefits of inflation, except that we can state with absolute certainty that they will also be lecturing us in the future on the evils and futility of seeking pay rises to compensate for inflation because these will only increase it. Not only will interest rates rise in response to higher inflation thus limiting the effect above, which will also put up the cost of mortgages, car loans and credit card debt etc. but higher inflation will also erode living standards. What workers might gain from erosion of the real value of the debt they will surely lose by the reduction in living standards caused by an increased cost of living.

By now it should be apparent that the deal’s main benefit is putting off repayment of the loan principal thus making it less likely the state will have to default. In other words the main beneficiaries are the State and the ECB, which is sanctioning the lending of the money and protecting the European banking system. What is good for the state, that it continues to pay and does not default, is bad for workers who will really do the paying.

The second benefit is that the low interest rate charged for the money the state gets in exchange for the bonds will be around longer. However as we have seen, how much longer we don’t know. It won’t be our decision when it goes up (through selling the bonds to the capitalists) because this is a decision of the European Central Bank. Such a decision will cost us billions but we have absolutely no say in the matter. Yes, we live in a democracy.

Once again it is necessary to educate workers that they must distrust the state as much as they would distrust an email from Nigeria asking for their bank details. (The power of the state means it doesn’t need them.) We need to remind them that the state is able to foist the debt of Anglo and Nationwide on them because it nationalised these institutions. We need to inform them that both the Irish Central Bank and European Central Bank are institutions of the state deliberately designed to be protected against any kind of democratic pressure.

This brings us to a couple of questions a reader asked me about the promissory note deal. He asks how the government borrows from the central bank as if it is separate institution. “To me it looks like the government is borrowing from itself, but if that is the case why doesn’t it borrow some more?”

The first answer is that with so much debt the Irish State cannot borrow more from the markets (private capitalist funds) which is why the EU and IMF stepped in to loan the money. It can’t borrow more from these institutions because they want the state to reduce its indebtedness and pay them back their existing loans.

The second answer is that the Irish Central Bank is a branch of the state and a normal central bank can both provide loans and ‘print money.’ There are limits to the former if, as we have just noted, the state won’t be able to pay the loan back. In this case it is if it makes a loan that isn’t repaid just printing money. Printing money will at some point lead to a devaluation of the currency meaning that the Euro will be worth less and buy less making everyone across the Eurozone worse off when it has to buy goods from countries that don’t sell in Euros.

To protect against this the ECB has a firm grip on money printing and the deal on the promissory notes and the new one involving the issuing of bonds required its approval. The Irish state is part of the Euro so doesn’t control its own currency or it could try to get away with printing some money, although in reality it is too weak to be able to do so even if it went back to the Punt.

The ECB is taking control of the timing of selling the bonds because printing money in exchange for bonds that don’t have to be repaid for years is so close to money printing it really is printing money.

The rules of the ECB prevent it funding states and public institutions directly for this reason. It has however ended up with Irish government bonds in exchange for funding the IBRC. Because it ended up in this position indirectly by funding a bank (public banks must be treated just like private ones)rather than a government and through the receipt at first of promissory notes rather than regular government bonds this has to a very little degree been hidden.

This is why they’re not very happy with the deal and might also be why they will quickly ensure the bonds are sold to private capitalists; thereby entailing an interest cost more reflective of the market. As I have said, this will cost the Irish people a lot of money.

In the next post I will look at whether the new deal has solved the debt problem.